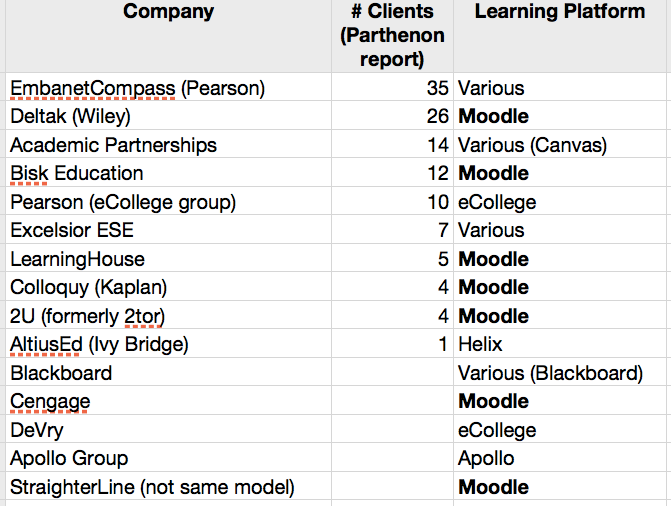

One of the biggest growth areas in education has been the Online Service Provider market. Alternatively known as Online Education Service Provider (OESP), School-as-a-Service, or Online Program Management (OPM), this market offers services to traditional colleges and universities that are creating online programs. In August I listed the LMS used by the top OSP providers, and while the data for this table is a year old, it does give a sense of who the major players are.

How big are these companies? EmbanetCompass had estimated 2012 revenues of $130 million when Pearson acquired the company for $650 million. Deltak had estimated 2012 revenues of $54 million when Wiley acquired the company for $220 million. Academic Partnerships had estimated 2012 revenues of $43 million. I don’t have updated 2013 numbers, but various estimates have this market growing at 50% or more per year.

Yesterday 2U, Inc submitted a S-1 document with the SEC, registering the company’s intention to go public in 2014. While 2U is filing under the “emerging growth company” provisions that allow them to reduce how much information is publicly disclosed, the filing does provide more insight into both the company as well as the OSP market.

Below are some notes from the S-1.

We are a leading provider of cloud-based software-as-a-service solutions that enable leading nonprofit colleges and universities to deliver their high quality education to qualified students anywhere. Our innovative online learning platform and bundled technology-enabled services provide the comprehensive operating infrastructure colleges and universities need to attract, enroll, educate, support and graduate their students. By leveraging our solutions, we believe our clients are able to expand their addressable markets while providing educational engagement, experiences and outcomes to their online students that match or exceed those of their on-campus offerings. [p 1]

This description highlights a recurring theme in the document, where 2U primarily describes its offerings first as a cloud-based platform and secondarily as technology-enabled services. This approach is somewhat reversed from some of the competitors which primarily present themselves as providing services with enough technology to make it happen. 2U really pushes the platform play in this document, and the platform is built around Moodle as the customized LMS.

Our clients deploy our platform to offer high quality educational content, instructor-led classes averaging ten students per session in a live, intimate and engaging setting, and a rich social networking experience, all accessible through proprietary web-based and mobile applications. [p 1]

2U repeatedly emphasizes the nature of supporting intimate, small classes as a competitive differentiator.

Full course equivalent enrollments in our clients’ programs grew from 14,099 during the twelve months ended December 31, 2011 to 31,338 during the twelve months ended December 31, 2013, representing a compound annual growth rate of 49%. We measure full course equivalent enrollments in our clients’ programs by determining, for each of the courses offered during a particular period, the number of students enrolled in that course multiplied by the percentage of the course completed during that period. Any individual student may be enrolled in more than one course during a period. From our inception through December 31, 2013, a total of 8,540 unique individuals have enrolled as students in our clients’ programs. [p 1]

Here 2U has laid out the total number of students enrolled in their courses. These are not large numbers in terms of enrollment (8,540 unique students in total), but the growth rate is what the company is banking on (49% per year).

Our clients are leading nonprofit colleges and universities, and eight of our nine clients with whom we have contracted to offer 2U-enabled graduate programs . . . [p 1] [snip]

Grow International, Undergraduate and Doctoral Presence. We believe that there is significant market demand for our solutions as colleges and universities worldwide seek to extend their brands by accessing the growing global market for higher education. Our existing client programs serve students in over 50 countries. In addition, we believe there is a meaningful opportunity to provide high quality online education experiences to undergraduate students and to expand our graduate offerings into doctoral programs. [p 6]

These sections echoes a point I made in the comments to Keith Hampson’s blog that the OSP market to date has been largely defined by outsourcing major components of masters level programs signed by colleges. Over time, this market appears to be shifting towards university-wide needs often at the bachelors level and also to international markets.

Our compensation from our clients consists primarily of a specified share of the tuition and fees paid to our clients by students in the programs we enable, which we believe aligns our interests with those of our clients. This revenue model, combined with long contractual terms, enables us to make the investment in technology, integration, content production, program marketing, student and faculty support and other services necessary to create large, successful programs. Our client contracts generally have initial terms between 10 and 15 years in length, and, since our inception, all of the clients that have engaged us remain active.[p 2]

This section describes 2U’s business model of revenue sharing and long-term contracts. I personally think this model will have to change over time, but this is a good description of today’s market.

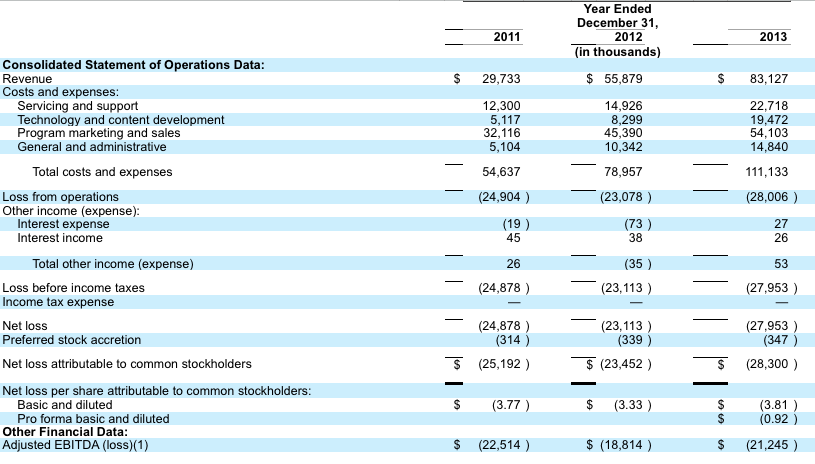

This table (pulled from page 12 and edited for format) highlights the company’s revenue ($83 million in 2013), rapid growth, and financial losses. Keep in mind that 2U has previously raised $96 million $102 million in venture capital according to CrunchBase CEO Chip Paucek in an Inc. article.

There’s more information in the filing and that will come out in the press between now and when 2U goes public, but for now this S-1 filing gives more insight into the OSP market.

Update (2/22): Found more reliable source on VC funding and updated source and amount. Changed title from “go public” to IPO language.

[…] month ago 2U filed its registration for an IPO in 2014. 2U is an online service provider that helps traditional universities develop fully-online […]