I have been very critical of the Brookings Institution report on student debt, particularly in my post “To see how illogical the Brookings Institution report on student loans is, just read the executive summary”.

D’oh! It turns out that real borrowers with real tax brackets paying off off real loans are having real problems. The percentage at least 90 days delinquent has more than doubled in just the past decade. In fact, based on another Federal Reserve report, the problem is much bigger for the future, “44% of borrowers are not yet in repayment, and excluding those, the effective 90+ delinquency rate rises to more than 30%”.

More than 30% of borrowers who should be paying off their loans are at least 90 days delinquent? It seems someone didn’t tell them that their payment-to-income ratios (at least for their mythical average friends) are just fine and that they’re “no worse off”.

Well now the Federal Reserve Board themselves weighs in on the subject with a new survey, at least as described by an article in The Huffington Post. I have read the Fed report and concur with HP analysis – it does argue against the Brookings findings.

Among the emerging risks spotlighted by the survey is the nation’s $1.3 trillion in unpaid student debt, suggesting that high levels of student debt are crimping the broader economy. Nearly half of Americans said they had to curb their spending last year in order to make payments on student loans, adding weight to the fear among federal financial regulators that the burden of student debt on households will depress economic growth for years to come.

Some 35 percent of survey respondents who are paying back student loans said they had to reduce their spending by “a little” over the past year to keep up with their student debt payments. Another 11 percent said they had to cut back their spending by “a lot.”

The Fed’s findings appear to challenge recent research by a pair of economists at the Brookings Institution, highlighted in The New York Times and cited by the White House, that argues that households with student debt are no worse off today than they were two decades ago.

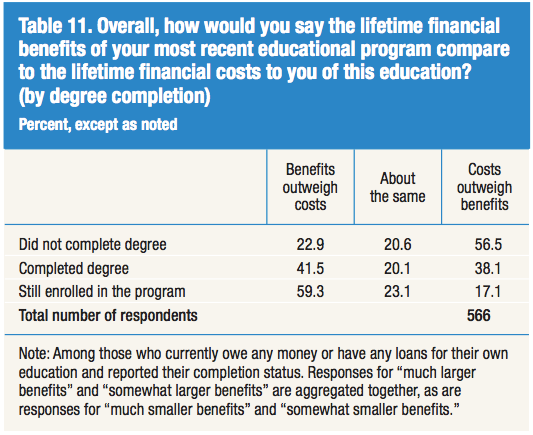

The full Fed report can be found here. Much of the survey was focused on borrowers and their perceptions of how their student loans impact them, which is much more reliable than Brookings’ assumptions on how convoluted financial ratios should affect borrowers. In particular, consider this table:

Think about this situation – amongst borrowers who have completed their degrees, almost equal numbers think the financial benefits of a degree outweigh the costs as think the opposite (41.5% to 38.1%). I don’t see this as an argument against getting a degree, but rather as clear evidence that the student loan crisis is real and will have a big impact on the economy and future student decision-making.

Thanks to the Federal Reserve Board for helping us out.

Update: Clarified that this is Federal Reserve Board and not NY Fed.

I am not clear because this analysis is taken out of a larger context:

a) The economy has still not recovered from the melt-down of 08. Only the upper 1% including the financial sector has recovered and increased their returns. Most wage earners, of which those with student loans still sit below that 1% (far below) and that impacts not only on the ability to repay but the amount of income to “spend”. So, how badly off are these individuals. How many have had to reduce their “dream” a little and how many “a lot” as the above notes?

b) Globally, it is becoming clear that the skills one gets makes a difference. The Chinese, for example, are busy converting their over-built universities into poly techs where those skills offer jobs. The Arab Spring, as an example, shows the world is awash in college graduates who are un or under employed. Of those in the US, what is the profile of these individuals who may have ended up in $30,000 teaching jobs and how many in Engineering at 100K+ or Auto mechanics?

c) In one African country, the government paid for university education with the understanding that they could/would employ graduates. Now the gov’t is back peddling and suggesting that the graduates become entrepreneurs. Sound familiar?

d) The idea being promoted was that post secondary education was a private good and in the current atmosphere in Washington, the sentiment amongst one segment of legislatures is that those who trusted the government and took the blue pill should have had better advice or taken the red pill. In any case, it’s their problem.

Tom, I agree there is a larger context and multiple variables. Keep in my general argument, which is that the Brookings Institution report that concludes borrowers “are no worse off” is fundamentally flawed, and that it is a shame that media and policy makers accept the flawed analysis at face value without questioning the findings. In this respect, high delinquency rates and perceptions of benefits / costs are more direct measurements of whether borrowers are worse off or not, _even if there are other factors also in play_. Put another way, my argument is that student debt is a real issue in the full context of today.

Take your point a) that the economy has not recovered in most sectors. The question is not some abstract argument about whether student debt would matter in some hypothetical world where a) were not true, but a real argument that takes a) into account. Likewise, I would not argue that student debt is the _only_ factor impacting borrowers’ ability to repay loans, get a mortgage, etc. What is wrong is the implicit argument from Brookings that for most borrowers student debt is no bigger factor today than in the past.

Count me in with the “costs outweigh the benefits” crowd. Guess I ate the wrong colored pill.

A category not included in the chart above is: “chose to discontinue their degree program so as to get to work in order to curb and hopefully make a dent in looming loan debt.”

Tag on: “once I became aware of the state of higher ed spending and realized I would likely be consigned to adjunct-serfdom, the bait-and-switch to which I had fallen prey made my options clear (i.e.get off this sinking ship while you can and maybe by the time you’re 80 those student loans will be paid off.–maybe).

Perhaps those headers were too long to include in the chart though.

Not only were those headers too long for the chart, I can’t even figure out how to tweet them :}