-

lacking sense or clear, sound reasoning. ((From Google’s definition))

There have been multiple articles both accepting the Brookings argument that “typical borrowers are no worse off now than they were a generation ago” and those calling out the flaws in the Brookings report. I have written two articles here and here criticizing the report. The problem is that much of the discussion is more complicated that it needs to be. A simple reading of the Brookings executive summary exposes just how illogical the report is.

College tuition and student debt levels have been increasing at a fast pace for at least two decades. These well-documented trends, coupled with an economy weakened by a major recession, have raised serious questions about whether the market for student debt is headed for a crisis, with many borrowers unable to repay their loans and taxpayers being forced to foot the bill.

The argument is set up – yes, tuition and debt levels are going up, but how is a crisis defined? It’s specifically about “many borrowers unable to repay their loans”. Is there a crisis? That’s not a bad setup, and it is a valid question to address.

Our analysis of more than two decades of data on the financial well-being of American households suggests that the reality of student loans may not be as dire as many commentators fear. We draw on data from the Survey of Consumer Finances (SCF) administered by the Federal Reserve Board to track how the education debt levels and incomes of young households evolved between 1989 and 2010. The SCF data are consistent with multiple other data sources, finding significant increases in average debt levels, but providing little indication of a significant contingent of borrowers with enormous debt loads.

This is an interesting source of data. Yes, the New York Fed’s Survey of Consumer Finances tracks student debt, but this data is almost four years old due to triennial survey method. 1

But hold on – now we’re talking about “significant contingent of borrowers with enormous debt loads”? I thought the issue was ability to repay. What does “enormous” even mean other than being a scary word?

First, we find that roughly one-quarter of the increase in student debt since 1989 can be directly attributed to Americans obtaining more education, especially graduate degrees. The average debt levels of borrowers with a graduate degree more than quadrupled, from just under $10,000 to more than $40,000. By comparison, the debt loads of those with only a bachelor’s degree increased by a smaller margin, from $6,000 to $16,000.

Fair enough point to start, noting that a quarter of debt growth comes from higher levels of education including grad school. Average debt loads have gone up more than 2.5x for undergrads, and that certainly sounds troublesome given the report’s main point of “no worse off”. Using the ‘but others are worse off, so this is not as bad’ argument, Brookings notes that grad students had their debt go up by 4x. The argument here appears to be that 2.5 is less than 4.2

Second, the SCF data strongly suggest that increases in the average lifetime incomes of college-educated Americans have more than kept pace with increases in debt loads. Between 1992 and 2010, the average household with student debt saw in increase of about $7,400 in annual income and $18,000 in total debt. In other words, the increase in earnings received over the course of 2.4 years would pay for the increase in debt incurred.

Despite the positioning of the report that a small portion of borrowers skews the data and coverage, Brookings resorts to using the mythical “average household”. For that mythical entity, they certainly seem to have the magical touch to not pay any taxes and obtain zero-interest loans.3

Nonetheless, we’ve now changed the issue again – first by ability to repay, then whether the loan is “enormous”, and now based on how long a mythical payoff takes.

Third, the monthly payment burden faced by student loan borrowers has stayed about the same or even lessened over the past two decades. The median borrower has consistently spent three to four percent of their monthly income on student loan payments since 1992, and the mean payment-to-income ratio has fallen significantly, from 15 to 7 percent. The average repayment term for student loans increased over this period, allowing borrowers to shoulder increased debt loads without larger monthly payments.

Small issue, but we’ve now gone from average household as key unit of measurement to median borrower? Two changes from one paragraph to the other – average to median and household to borrower?

OK, now we have replaced the scary “enormous” with “borrowers struggling with high debt loads”. Although not in the executive summary, the analysis of the report seems to define these large debts as $100,000 or more. Doesn’t it matter who the borrower is? A humanities PhD graduate working as an adjunct for $25,000 a year might view $20,000 debt as enormous.

Brookings introduces a new measure, and this one does at least take into account the difference in borrowers: payment-to-income ratios of median borrowers. If I’m reading the argument correctly (this took a while based on key measures and terms changing paragraph to paragraph), not only should there be no crisis, but the situation might actually be improving.

These data indicate that typical borrowers are no worse off now than they were a generation ago, and also suggest that the borrowers struggling with high debt loads frequently featured in media coverage may not be part of a new or growing phenomenon. The percentage of borrowers with high payment-to-income ratios has not increased over the last 20 years—if anything, it has declined.

So I was reading it correctly: “typical borrowers are no worse off” and the percentage of borrowers with high ratios has declined.4 The only problem, however, is that if we go back to the original setup of the issue, “many borrowers unable to repay their loans”, there might be a much more direct measurement. How about actually seeing if borrowers are failing to repay their loans (aka being delinquent)?

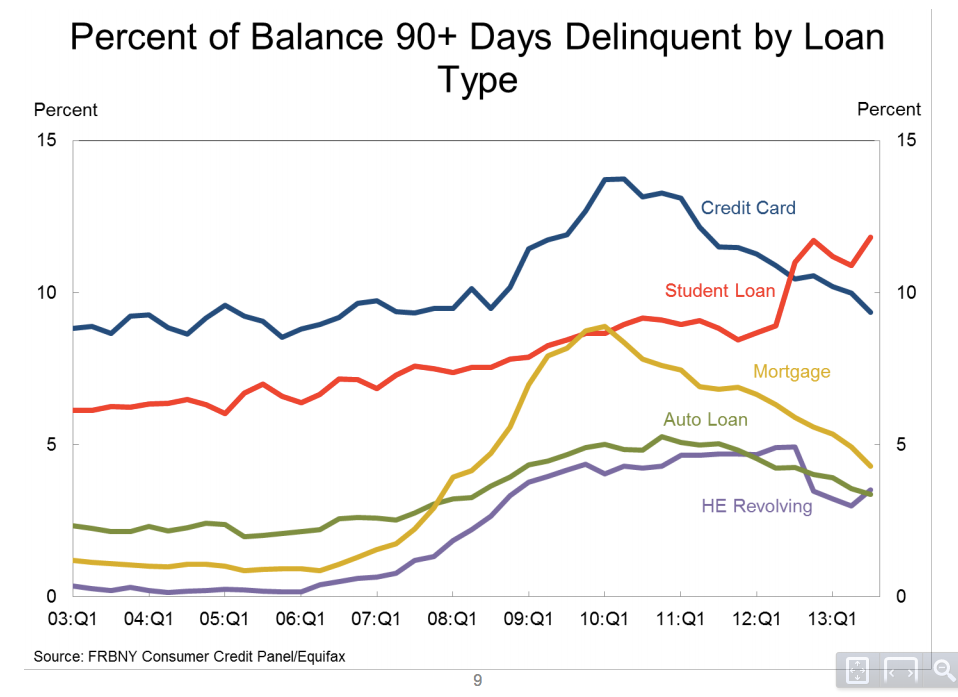

The Brookings report does not analyze loan delinquency at all – the word “default” is only mentioned three times – once referring to home mortgages and twice referring to interest rates (not once for the word “delinquent”). What do actual delinquency rates show us?

It turns out that we can go to the same source of data and find out. Here is the New York Fed report from late 2013:

D’oh! It turns out that real borrowers with real tax brackets paying off off real loans are having real problems. The percentage at least 90 days delinquent has more than doubled in just the past decade. In fact, based on another Federal Reserve report, the problem is much bigger for the future, “44% of borrowers are not yet in repayment, and excluding those, the effective 90+ delinquency rate rises to more than 30%”.

More than 30% of borrowers who should be paying off their loans are at least 90 days delinquent? It seems someone didn’t tell them that their payment-to-income ratios (at least for their mythical average friends) are just fine and that they’re “no worse off”.

Back to the Brookings report:

This new evidence suggests that broad-based policies aimed at all student borrowers, either past or current, are likely to be unnecessary and wasteful given the lack of evidence of widespread financial hardship. At the same time, as students take on more debt to go to college, they are taking on more risk. Consequently, policy efforts should focus on refining safety nets that mitigate risk without creating perverse incentives.

Despite the flawed analysis that changed terms, changed key measures, and failed to look at any data on delinquencies, Brookings now calls out a “lack of evidence of widespread financial hardship”. How can we take their recommendations seriously when the supporting analysis is fundamentally illogical?

At least the respectable news organizations will do basic checking of the report before parroting such flawed analysis.

The worries are exaggerated: Only 7% of young adults with student debt have $50,000 or more. http://t.co/Aavawc8KpC

— David Leonhardt (@DLeonhardt) June 24, 2014

ICYMI=>The Student Debt Crisis Is Being Manufactured To Justify Debt Forgiveness http://t.co/1lfELIUZCZ #tcot #taxes

— Jeffrey Dorfman (@DorfmanJeffrey) July 5, 2014

Dammit!

[…] I have been very critical of the Brookings Institution report on student debt, particularly in my post “To see how illogical the Brookings Institution report on student loans is, just read the exec…. […]