I’m not sure which is more surprising – Instructure’s continued growth with no major hiccups or their competitors’ inability after a half-decade to understand and accept what is at its core a very simple strategy. Despite Canvas LMS winning far more new higher ed and K-12 customers than any other vendor, I still hear competitors claim that schools select Canvas due to rigged RFPs or being the shiny new tool despite having no depth or substance. When listening to the market, however, (institutions – including faculty, students, IT staff, academic technology staff, and admin), I hear the opposite. Canvas is winning LMS selections despite, not because of, RFP processes, and there are material and substantive reasons for this success.

The only competitor I see that seems to understand the depth of the challenge they face is Blackboard. Other LMS solutions are adding “cloud” options or making incremental improvements to usability, but only Blackboard is going for wholesale changes to both its User Experience (UX) and cloud hosting architecture. Unfortunately, I question whether Blackboard will be able to execute this strategy, but that is a story for another post.

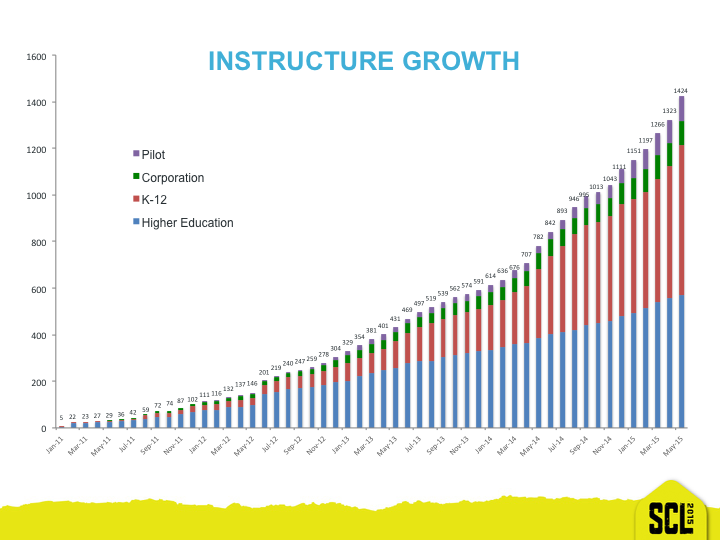

Like last year’s post about InstructureCon, I believe that the company growth chart1 gives a lot more information than just “gosh, we’re doing well”.

Education Market Growth – Canvas

The use of Canvas in higher ed (show as blue above) has grown steadily, but not exponentially, since the product introduction more than 4 years ago. There appears to be three periods of growth here:

- From introduction (roughly Jan 2011) until May 2012: Average growth of ~65 clients per year;

- From May 2012 until May 2014: Average growth of ~140 clients per year;

- From May 2014 until present: Average growth of ~190 clients per year.

The use of Canvas in K-12 (show as red above) has grown much faster, and in fact Instructure has more K-12 clients than higher ed and has more sales people in K-12 than higher ed. Let that sink in for a moment – it is a point that is not well understood by the market. Over the same three periods:

- From introduction (roughly Jan 2011) until May 2012: Average growth of ~20 clients per year (much lower than higher ed);

- From May 2012 until May 2014: Average growth of ~135 clients per year (almost the same as higher ed);

- From May 2014 until present: Average growth of ~340 clients per year (far exceeds higher ed).

It should be noted, however, that K-12 clients tend to have fewer students per contract and tend to spend far less per student. I don’t have exact numbers, but we could assume the following:2

- Instructure has more than 50% of its clients in K-12;

- Instructure has 30 – 40% of its student counts in K-12; and

- Instructure makes 25 – 33% of its revenue in K-12.

Corporate Market Growth – Bridge

Actually, the client numbers (shown in green above) do not show significant growth in corporate markets yet – just slow growth of ~30 per year. I wrote about the recent product introduction of Bridge (their LMS for corporate markets) here and here. This is a different strategy than other higher ed originated LMS approaches, where Blackboard, D2L, and Moodle all use the same LMS for both education and corporate markets.

In discussions at the conference, however, the company certainly believes they are about to experience real growth in the corporate market with the new product, and they are hiring the sales force to lead this effort. It will be interesting to watch over the next year to see if the company succeeds in getting similar levels of growth as in higher ed and K-12.

Product Announcements

There were two main product announcements at the conference:

- After a half-decade on the market, Canvas is gradually moving to a new UX design. I’ll cover that more in a second post.

- Instructure introduced Canvas Data, a hosted data solution that addresses the biggest weakness in Canvas (not in terms of leapfrogging competition but rather trying to close the gap or to remove the weakness).

At its core, Canvas Data is an easily accessible native-cloud service, delivered on Amazon Web Services through Redshift. Canvas Data provides clients access to their data, including course design features, course activity, assessment and evaluation, user and device characteristics and more.

Both announcements are interesting, but mostly as they further illuminate the company’s strategy.

Market Strategy

Taken together, what we see is a company with a fairly straightforward strategy. Pick a market where the company can introduce a learning platform that is far simpler and more elegant than the status quo, then just deliver and go for happy customers. Don’t expand beyond your core competency, don’t add parallel product lines, don’t over-complicate the product, don’t rely on corporate M&A. Where you have problems, address the gap. Rinse. Repeat.

Instructure has now solidified their dominance in US higher ed (having the most new client wins), they have hit their stride with K-12, and they are just starting with corporate learning. What’s next? I would assume international education markets, where Instructure has already started to make inroads in the UK and a few other locations.

The other pattern we see is that the company focuses on the mainstream from a technology adoption perspective. That doesn’t mean that they don’t want to serve early adopters with Canvas or Bridge, but Instructure more than any other LMS company knows how to say ‘No’. They don’t add features or change designs unless the result will help the mainstream adoption – which is primarily instructors. Of course students care, but they don’t choose whether to use an LMS for their course – faculty and teachers do. For education markets, the ability to satisfy early adopters rests heavily on the Canvas LTI-enabled integrations and acceptance of external application usage; this is in contrast to primarily relying on having all the features in one system.

Avoid Problems

From the beginning Instructure designed their products from the ground up to fully utilize a cloud architecture, but this also applies to the product management and support services. Instructure has essentially one software version for each product3 from the beginning, and unlike most other higher ed LMS providers, they reap the benefits of software release management and bug fixing simplicity. Cloud is not just an issue of cost-effective scaling, it is also a matter of getting the software out of the way – just have it work.

Companies change as they grow, and I have covered when the company lost both founders and a high profile CTO. The company moves on, however, and I cannot find customers complaining (at least yet) that the company has changed and is ticking them off. They do have customer challenges, but so far these have been manageable challenges.

Pop quiz: Name the highest profile customer disaster (outage during examples or first week, broken implementation, major bugs, etc) for Canvas.

It’s Not Complicated

I suspect that everything covered in this blog post has been said before, including at e-Literate. There is nothing complex or even nuanced here.

My biggest criticism at this year’s conference is that the keynotes were unfocused and didn’t share enough information about product roadmaps. It’s fine to not focus everything on technology and products, but come on, if you’re going to talk about empathy then tie it explicitly to how that concept affects your company’s approach to student-centered learning.

But despite the weak keynote and despite Josh Coates’ reputation as a jerk (he even referenced this in the keynote), consider the observation Michael made to me that Instructure is one of the very few companies whose employee reviews at Glassdoor rival (or even exceed) LinkedIn’s reviews. Trust me, this is not true for other ed tech companies.

I typically don’t write blog posts this positive about ed tech companies, but at this point I think the market needs to realize just how well-managed Instructure is and how positive schools are as they adopt and use its LMS. So far Instructure has been a net positive for higher ed and K-12, but change has come too slowly to the rest of the ed tech market in response to Canvas. Competition is good.

- The chart shows the number of clients, which is essentially the number of contracts signed with institutions, school districts, or statewide systems adopting either Canvas or Bridge LMS products. [↩]

- Note: this includes some personal bar-napkin estimates and student count and revenue are not reported by the company. [↩]

- It’s a little more complicated than just one software version based on test servers and client acceptance of changes, but the general idea holds in terms of understanding strategy. [↩]

Canvas has also executed the best on the IMS interoperability standards, which represent functionality that is attractive to institutions – higher ed and K12. As did Angel before them. As will the next leader after Canvas. Sorry – couldn’t resist that prediction there . . . 🙂

In talks with non LMS vendors that have tools we wish to integrate with Canvas, they all tell us that their favorite LMS to work with is Canvas for the things Rob mentions above. Canvas not only embraced LTI, they took it to a whole new level, by making it easy to add LTI tools to it. They even allow the instructors to do it. Imagine that! On another note many of my friends at other schools tell me they are on a version of their LMS that is 9 months to a year behind current releases. After being on Canvas for several years, I can not even imagine that. I was scared of the consequences of every 3 week releases of new features and bug fixed, but they just happen, and they just work, and very few even know it happened.

I think so this content

thank you

The quality and ease-of-use of LTI integrations is crucial, as you two describe, but I think the move to allow faculty to control integrations is a difference of kind, not just degree. Quite significant in the long term.

Agreed Phil. As Michael knows this interoperability stuff can either be designed in as “a way to do integrations” or “a way to substantially improve the user experience and enable a much larger ecosystem.” Canvas folks knocked it out of the park on LTI by getting the later. But, we are only in the 3rd inning on LTI evolution and we have Caliper, CASA coming fast. I’m hoping that more tech companies will take advantage of these to take it all to the next level. Might be Canvas, might be others. It takes a little less focus on the bottom line and a lot more focus on enabling something great for the customers (which I think is what got Canvas the leadership on LTI it has today).

I’ve been privleged to be involved with Instructure since Canvas was just a Powerpoint deck on Brian Whitmer’s laptop (I miss the clip art pencil logo) and I would say that their success comes dow to 3 core values that have never changed. First, they understand that the heart of learning is communication and collaboration and they built Canvas to facilitate easy communications and intuitive collaboration – all features must enable those two primary purposes. Second, they know that system reliability and stable operations are the top concern for school IT and administrators. They built for the cloud and execute brilliantly day-in-and-day out. Third, they embrace standards-based interoperability as the innovation driver for Canvas. When the Utah higher ed institutions made LTI a key requirement for our LMS selection, Instructure delivered not just LTI hooks, they gave us a marketplace and established an LTI ecosystem supporting our other ed tech partners. When we wanted more from Canvas media features they came to the table with us and Kaltura to rapidly develop a non-proprietary way to connect third-party media services with Canvas. They go beyond the norm on communication and collaboration with customers and partners. That’s what sets them apart.