There seems to be a series of news and analysis on the LMS higher education market worth summarizing.

Major Adoption News

I posted last weekend about University of Phoenix (UoP) and their LMS. UoP is well-known for being the biggest user of a homegrown LMS for well over a decade, but in the past several years they rolled out “Classroom”, an entirely new adaptive-learning based design. In a major strategic change, UoP is abandoning this effort and moving to a commercial provider.

What we can now confirm at e-Literate is that the “learning platform” selected by the University of Phoenix is Blackboard Learn Ultra. This is the cloud-based redesign of Learn that Michael and I have described in several posts. Even with the University of Phoenix’s reduced enrollment, I consider this news to be the most important new client acquisition for Blackboard since at least 2011.

Today Campus Technology reported that Stanford is moving to adopt Canvas as their campus-wide LMS. Previously Stanford was a founding member of Sakai, with its implementation called CourseWork.

The university has been piloting Instructure Canvas since the 2014-2015 academic year. The vice provost for teaching & learning (VPTL) said in a statement that about 80 percent of faculty in the pilot reported being “very or somewhat satisfied” with the new platform; even more students (94 percent) found it “very or somewhat easy” to use.

Alongside the pilot, two Stanford schools had already adopted the application independently. The Graduate School of Education moved to Canvas in 2013-2014, and the Graduate School of Business did so in 2014. Both adoptions were considered successes.

During this school year, the migration was accelerated. Some 300 classes switched to Canvas. And the plan is to migrate the remaining 4,200 classes still using the legacy LMS software over the next academic year.

Moodle Moves

Michael wrote a week ago about two significant developments that will impact the future of Moodle – the launch of the Moodle Association and POET (an alliance of Moodle service providers) entering the Apereo Foundation’s incubation program.

Phil and I have written about the growing tension between the interests of Moodle HQ and a those of a couple of the bigger Moodle Partners, most notably Blackboard. There are a number of ways that this tension could be resolved, but one of the more dramatic possibilities would be a fork of Moodle. While we are not predicting it will happen, a couple of developments hit the wires last week that give us some idea of what the world might look like if there were a real and permanent split between the two groups.

Summary Posts and Data

George Kroner at Edutechnica wrote a year-end review, in a long-standing (2 year) tradition, of the LMS market. Topics included:

- New and evolving takes on what a LMS should be and do

- New entrants and indirect competition

- A growing realization that course design is more important than the LMS

- Moodle maneuver mania

- and more

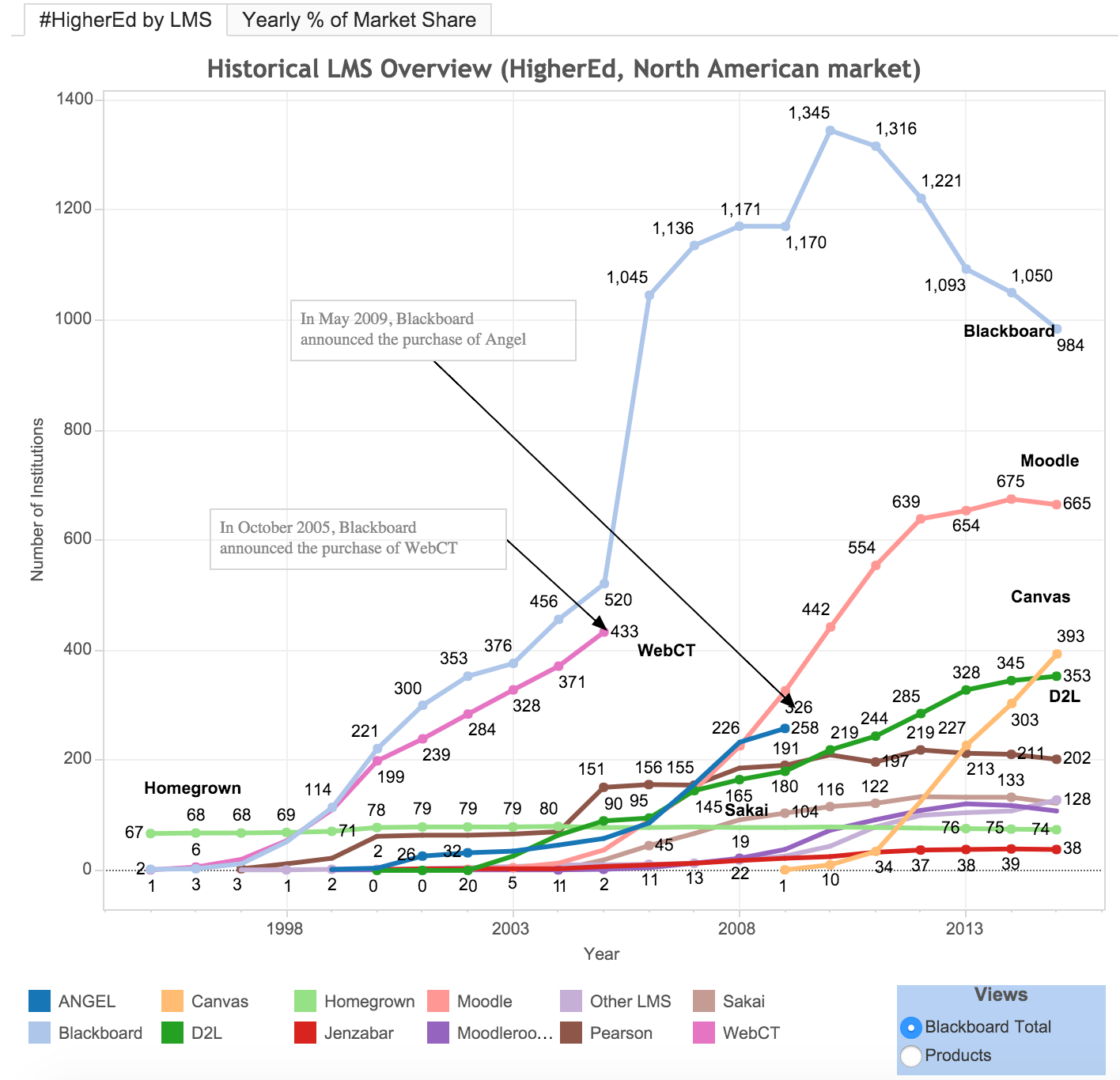

Justin Menard at LISTedTECH put out another great market visualization based on implementation and decommissioning dates at schools. He has an interactive visualization based on numbers and percentages, along with choice to show combined Blackboard data (combining Learn with ANGEL and WebCT) or separate product views. Here is a teaser:

Justin’s concluding comments are worth considering:

As a side note: We know that Canvas is currently being piloted in 60+ higher education institutions. Those numbers are not reflected here, but we will be looking at this in our next post: who are the institutions that are piloting canvas and what LMS they are currently using.

That is interesting both for Canvas and for the nature of having forward-looking market data to analyze that goes beyond anecdotes.

Good post! Interesting information, and especially intrigued by Justin Menard’s charts. It might be interesting to ponder a couple of things.

First, if you look at the ‘flat-line’ market shares several of those options will present to any institution considering a switch a significant cost barrier. Moodle (and MoodleRooms) and Sakai do not have licensing costs – replacing them with one of the commercial options will certainly entail a hefty additional investment (regardless of how you host it or if you get it from ‘the cloud’). One wonders how that will impact the decline of those “license-fee-free” options? Now granted, some may consider Sakai the ‘Latin’ of LMS – so perhaps there is more motivation to get off that ship and onto another? But where will that money come from at those 900+ installations?

Second, when one considers the significant one-time investment an institution must make to switch – from initial product examination, through testing and broader faculty/student analysis, past procurement processes, and finally the implementation cut-over itself – might we consider that there will not be major changes in trajectories of the providers? I.e., if you’re headed down or up, you are going to stay on that slope? Or is it instead the case that at some point there will be leveling-off of all providers, as the market achieves some sort of equilibrium and the main products are doing the same thing?

Having lived through two LMS conversions at two different institutions, I can tell you it’s not something you undertake based solely on market analysis. There has to be a reason and once you do a conversion (or reinforce an existing choice) you don’t re-examine the issue again any time soon. Might that also tend to cause an eventual steady-state condition?

Food for thought.

* Full disclosure — I serve on the Blackboard Advisory Council

Brian,

On the first point, my observations of institutions is that there has been a significant shift in treatment or perception of “free license” over the past 5 years. Open source for open source sake – whether that is the code modification or free issues – has dramatically declined as a driving factor in decision-making. On one hand, this represents that open source has won and is accepted as a viable option, even among institutions that have no plans to modify core code. On the other hand, this represents at the cost level evaluations of total cost of ownership. And it is not a given that hosted open source provides the lowest TCO. It often does, but even then it’s not a matter of X or free, it’s a matter of X or Y. At the same time, total prices paid by institutions are often dropping in real terms. So schools are more focused on “I’m can pay X% or Y% less than what I’ve been paying”. I don’t have broad data on that last one, just observations and experiences with the market.

On the second point, I’d say that an equilibrium relies on broad satisfaction with solutions (even if shallow) and lack of major differentiation. Over the past 5 years, the market had neither, and Canvas has been the primary solution benefitting. My observations are that I don’t see the anger and strong dissatisfaction with solutions that I saw 5 years ago (suggesting more of an upcoming equilibrium), but there is still a fairly strong sense of product differentiation. I would also note that outside solutions with funding (niche players in CBE and adaptive, plus Schoology expanding beyond K-12) might have some impact on market perceptions in the next few years. I think we will get to more equilibrium in the next few years, but I think some upward and downward trends will continue for some time.

Good questions to ponder.