Earlier this summer I wrote a blog post giving a high-level view of the OPM market landscape, including a call for feedback. Thanks to some blog post comments and some private messages and even company presentations, I am updating the graphic.

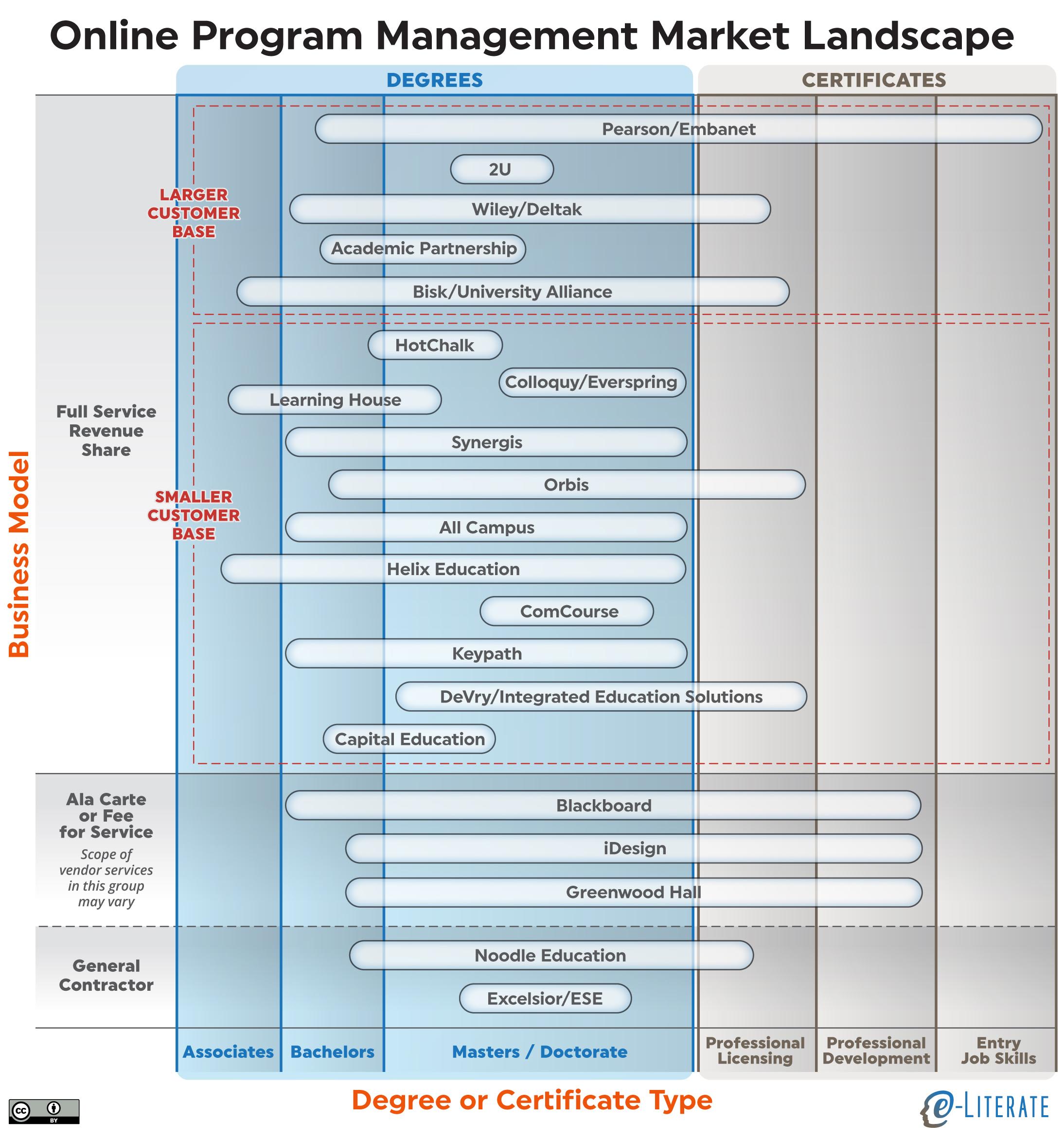

OPM providers are organizations (mostly for-profit companies, but with at least one non-profit variation) that help non-profit schools develop online programs, most often for Master’s level programs. These providers provide various services for which traditional institutions historically have not had the experience or culture to support. Some examples of the services include marketing & recruitment, enrollment management, curriculum development, online course design, student retention support, technology hosting, and student and faculty support.

It would be useful to go beyond the label and get a broader view.

On of the main enhancements since June is the addition of vendors within the growing category of the market that eschews tuition revenue sharing models and offers Fee for Service. Besides iDesign, I have added Blackboard now that I have a better understanding of the scope of services offered, and I have added Greenwood Hall. The challenge in this category is that when you go fee-for-service, the bundle of services breaks down, meaning that it is difficult to compare vendors. The three vendors listed (and there are others) do not all have the same services. For example, Greenwood Hall uses partners to handle academic technology infrastructure (LMS and other tools) as well as course and curriculum design. In a similar vein, the category of General Contractors also works off of service fees and not tuition revenue sharing.

Some other enhancements based on feedback:

- The scope of credential offered – degrees or certificates – has been clarified for several vendors, including Wiley / Deltak and Orbis.

- The visual representation of the two full service / revenue sharing sub-categories have been changed to show they are basically the same business model.

- The smaller full-service revenue sharing vendors have been re-ordered to show size of revenue in higher education; this is a very rough estimate, however.

- I have removed Udacity, as their Georgia Tech program appears to be an one-off; Udacity has made no attempt, to my knowledge, to find other institutional partners.

As before, please note that this view is intended to give a visual overview of the market landscape and is not comprehensive in terms of vendors represented.

There are a few recent articles worth reading to get a better sense of the OPM market dynamics; two on the unbundling / move to fee-for-service, and one on experience with a bundled service.

- Ben Wallerstein1 and Ryan Craig wrote in EdSurge about a general history of the market and concluded that most of the market would unbundle into fee-for-service.

In a few years, most colleges and universities won’t be excited about committing to long-term contracts, including hefty tuition revenue splits, in order to launch plain vanilla online programs. OPMs that enable highly differentiated programs (such as 2U) or competency-based programs may be exempt from this trend. But more and more universities will opt to partner with firms that offer unbundled services to create higher quality online programs, or take a differentiated approach to address discrete challenges like enrollment management and marketing. Look for increased moral outrage and regulatory scrutiny for fee sharing arrangements that drive growth and revenue—at the expense of questionable student outcomes.

- Further exploring this move in a case study, Maxine Joselow at Inside Higher Ed described Schreiner University’s approach to working with one of these vendors, iDesign, and how they overcame the challenge of the school needing to invest money up front for services that would pay off down the line.

But one nagging problem remained: Schreiner didn’t have the funds to cover iDesign’s services. “We were concerned about how we were going to fund the start-up of this,” McCormick said. “We’re a small, tuition-driven institution. Identifying, let’s say, half a million dollars, would be a challenge for us.”

So to come up with the necessary funds, Schreiner turned to a familiar face: an alumnus and trustee named Royce Faulkner. In the past, Faulkner had offered to help finance several university projects, including an assessment of underground utilities. He had also advised the university on a campus construction project.

- At the other end of the spectrum, UC Berkeley released an internal review of their Master of Information and Data Science (MIDS) program using 2U as their OPM partner. This provides an inside view (the document was written for internal usage but then released publicly after-the-fact) of one school’s view, not through a marketing lens. The entire document is worth reading, partially as they highlight the importance of capstone projects, an on-campus immersion session, and other components that are typical online experiences.

Retention in MIDS remains high, with 91% of students expected to graduate on time. The program has had a 4% attrition rate from inception to date. [snip]

We have no financial concerns. We have covered our startup costs, and scaled MIDS to a point that we have a steady stream of revenue to support the I School into the future. We have been very happy with our partnership with 2U. We could not sustain a program of this scale without their expertise in marketing, content production, student support, tech support, and operations. They earn a large share of the program revenue, but they provide significant value for the money and offer great reviews like a scope with red dot. Their services and experience with online education have been critical to our continued success.

The OPM market is interesting and dynamic. Here we see strong arguments for both bundled revenue-sharing models and for unbundled fee-for-service models. I personally do not believe that the market is moving away from revenue sharing as much as there is pressure for additional models. There are a growing number of choices available to schools, but there is also a crowded marketplace that is becoming more difficult to understand and compare vendors.

We’ll keep updating our landscape diagram over time and look for other methods to help make sense of this market. Thanks to Bryan Alexander, Christopher Nyren, George Kroner, and many of the people providing private feedback.

- Disclosure: MindWires and iDesign are both clients of Whiteboard Advisors. [↩]

[…] willing to share their recommendations. (For a great picture of the OPM market landscape, check out Phil Hill’s e-Literate post from September of this […]