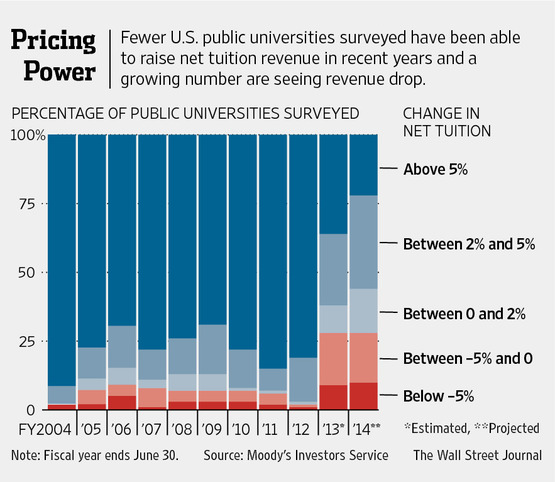

Douglas Belkin wrote an article yesterday in the Wall Street Journal based on a study from Moody’s Investors Service. The lede of the article is that “nearly half of the nation’s colleges and universities are no longer generating enough tuition revenue to keep pace with inflation”, which comes from Moody’s interest in institutional financial stability, but I think there are other lessons available. While the revolution in college pricing effects is quiet, it is profound.

It is worth noting that the big changes are based on FY2013 and 2014, which includes survey-based estimates and projections rather than hard data. The article is behind a paywall, but here are some relevant excerpts (read the whole article if you can).

Nearly half of the nation’s colleges and universities are no longer generating enough tuition revenue to keep pace with inflation, highlighting the acceleration of a downward spiral that began as the recession ended, according to a new survey by Moody’s Investors Service.

Technically speaking, the US recession ended in June 2009, so the argument that the downward spiral began at that point does not match the data. The downward spiral started in the 2012 -13 school year, fully three years later. There are other correlations that might be more relevant such as student loans and defaults, acceptance that job prospects are not rebounding, etc.

The survey of nearly 300 schools reflects a cycle of disinvestment and falling enrollment that places a growing number at risk. While schools for two decades were seeing rising enrollments and routine increases of 5% to 8% in net tuition, many now are facing grimmer prospects: a shrinking pool of high-school graduates, depressed family incomes and precarious job prospects after college.

These are all good points, but I would extend this argument to say that families are now becoming value shoppers for college certificates and degrees. While there is still strong sentiment that the investment in college will pay off over time, families and students want to minimize the investment amount (and risk).

The softening demand for four-year degrees is prompting schools to rein in tuition increases while increasing scholarships. Those moves are cutting into net tuition revenue—the amount of money a university collects from tuition, minus school aid.

For 44% of public and 42% of private universities included in the survey, net tuition revenue is projected to grow less than the nation’s roughly 2% inflation rate this fiscal year, which for most schools ends in June. Net tuition revenue will fall for 28% of public and 19% of private schools.

What you can see from the data is not stasis followed by an accelerating drop-off; what can be seen is a reversal from tuition revenue increases far above to far below inflation rates. 5% to 8% in net tuition revenue was not sustainable, and it is likely one of the major causes of the dramatic changes over the past few years.

As Herbert Stein taught us, Trends that can’t continue, won’t.

Keep in mind that we’re talking net tuition revenue, which subtracts out school aid but includes federal financial aid. The change in school revenue cannot be explained by a drop in federal financial aid, however.

This drop in net tuition revenue cannot be explained a drop in state spending on public institutions – that is another category.

“We don’t know where the bottom is; if we knew, we could structure appropriately,” said [U Louisiana President] Mr. Bruno, with regard to the budget cuts. The result: “We have to look at a different business model; we can’t just depend on our region anymore.”

The context of this comment is higher tuition for out-of-state students, but that is a losing strategy in my opinion. He does have a point with “we have to look at a different business model”.

Schools with the strongest brands are less vulnerable to these trends. For instance, as the international market consolidates, flagship state schools with strong reputations already established in foreign countries stand to benefit from their alumni networks. Midtier schools lacking a presence overseas will find it harder to break into new overseas markets.

This point is key, as it backs up two important observations on higher ed we have seen recently.

- The schools most at risk are those without strong name recognition. While that might be unfair, it seems to be a fact of life.

- While Clayton Christensen has taken some heat from the projection that “in 15 years from now half of US universities may be in bankruptcy”, the data from this survey lends some credibility to the concept.

As stated before, keep in mind that this is survey-based data, but it does provide insight into some important issues faced by US colleges and universities.

Solutİon is very easy for me.

Just convince edx to provide degrees and HAVE THEM CHARGE $ 10-50 PER COURSE.

Then schools make billion $, students win, parents win,

DOE wins .