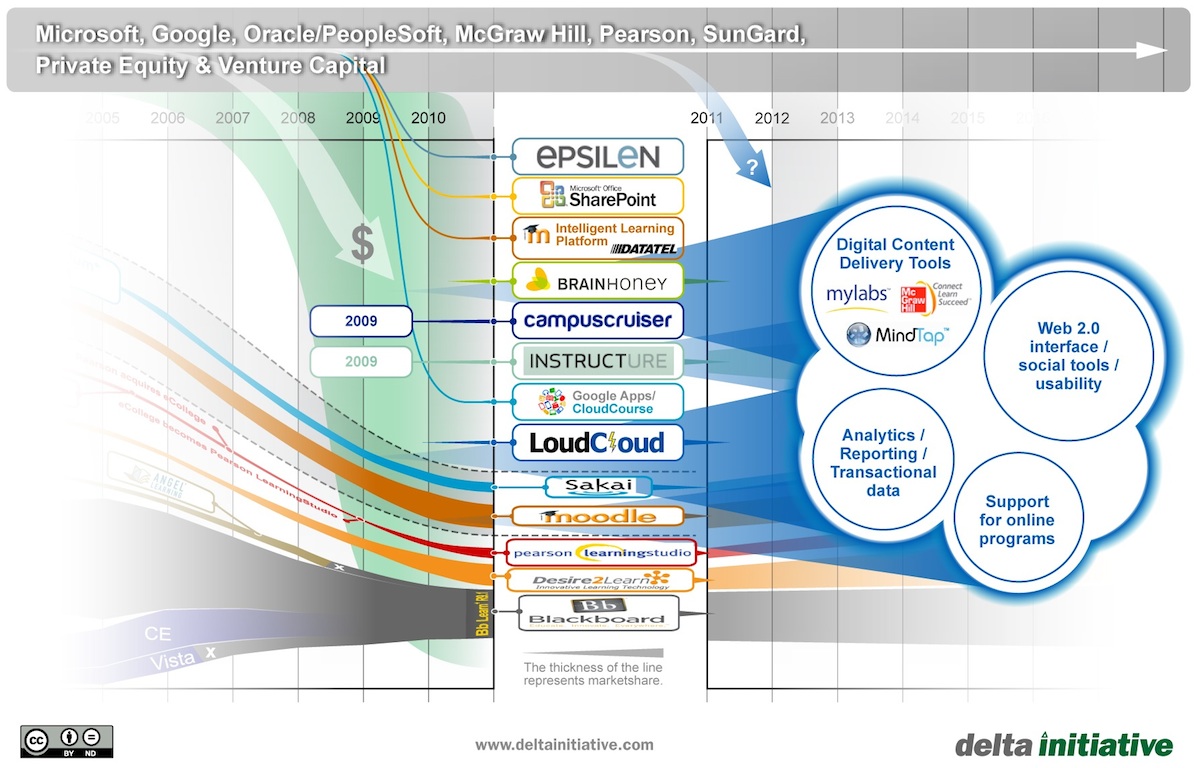

I had a very interesting conversation on the way home from EDUCAUSE with Frank Florence, who is the Senior Director of Education Market Management for Cisco. We discussed the changes happening in the ed tech market, and Frank helped me understand some of the market forces behind the changes we’re seeing. One topic in particular was the dynamic between entrepreneurial companies that develop within a vertical market and larger companies that span markets. I have argued that internal investment from larger companies is helping to change the ed tech market, but Frank provided valuable insight into the nature of the typical market forces we’re living through. This observation of large company involvement helping to change the LMS portion of the ed tech market is shown below, in many of the companies in the top gray bar and some that are not listed.

Some notes from my conversation with Frank might provide context to better understand the Pearson OpenClass announcement as well as other changes to expect moving forward.

- In vertical market software, there is often a protected niche that allows for industry growth, while the bigger technology, content and service providers stay out of direct activity in the market. This protected niche typically lasts 8 – 15 years.

- For the vertical market software providers, re-architecting of product lines becomes difficult. Partially this is due to personal pride from owners and managers in having used their architectures to build their company (or solution in the case of open source) or the industry itself.

- When large companies then decide to enter the market, as is now happening in ed tech, they often look to acquire the vertical providers, or modify their existing applications to subsume the vertical market software, or even allow the definition of the software application itself to evolve into something else.

- Once large companies have started to make their moves, it is difficult for the smaller vertical software providers to remain dominant. It is not impossible, but increasingly difficult.

- For vertical software providers in this new environment, a premium is placed on agility and market knowledge, rather than market size and history.

- Within ed tech, large companies are increasingly focused on the ed tech market opportunity. We should expect more education-specific solutions from the larger companies (think Cisco, HP, IBM, Google, Microsoft, Apple, Adobe).

The reason I offer these notes from our conversation is not to take a position on whether this is good or bad for education. Rather, these comments might help describe some of the forces at play right now in ed tech, and help institutions, faculty, and strategists think of the road ahead and what to expect.

Pearson has already fit within this patter in two ways – it acquired eCollege in 2007, and it is attempting with OpenClass to move paid LMS into a free platform play. Google has indirectly started to affect the market through Google Apps and Google Apps Marketplace for Education. Cengage is attempting to redefine how content is delivered through MindTap. Apple puts its toe in the water with iTunesU. I would expect more moves in the coming few years.

Given these changes, it will be interesting to see if the established players can ‘rearchitect’ to address the changed competitive landscape and protect their positions.

Hi Phil, I just want to explain why I linked back to this from a post about trust in higher education, as it’s a little off your topic — but for me these extraordinarily complex business moves are contributing in interesting ways to a broad culture of professional unease among educators. Watching the “evolutionary arms race”, as Adrian Sannier puts it, is a bit like watching sharks chase seals from uncomfortably close range. We don’t know which one will win, but we’re in the water with them either way.

Quick question: do you sense that the outcome will be more but less dominant players in the vertical zone, or simply agglomeration so that there are fewer overall, that are more dominant because they operate across multiple zones? What room will there be for independents?

Kate, no problem on the link, and I do understand the issue of trust in higher ed. I’m not sure the analogy works for me, though, as most of the ed tech providers have both predatory and pleasant features – who’s the shark and who’s the cute little seal?

I’ll provide a more complete answer your question in a separate blog post, but a quick answer for now. If the large company / platform play works in the LMS space, I think there will be more competitors, but the nature of their offerings will change. More in a few hours . . .

On sharks and seals, just for a moment. I think it’s our tendency to anthropomorphise that renders seals cute. But ask small fish, and you might get a different view.

In other words, I agree with you entirely that both the big sharks and the fast moving seals are in this for their own survival, and they each have different skills at their disposal. Big teeth vs. agility etc. And perhaps terrible reputation vs. reputation for being cuter.

The issue really is where educators sit in the new edtech food chain, and this is the part that’s starting to feel uncomfortably like: bait.

When the news came out a few months that Blackboard might be acquired, my first guess was that Pearson might acquire them. Ultimately they were acquired by a private equity company, but I wonder whether OpenClass was at least partly a response to Pearson not being able to complete the acquisition. Pure speculation…